If you are hit by an uninsured driver, your ability to recover compensation depends entirely on your own insurance coverage. Without UM/UIM coverage in place, there may be little to no insurance recovery available for your injuries and damages. Having UM/UIM coverage is what provides a potential source of compensation when the at-fault driver has no insurance or insufficient coverage.

Uninsured motorist (UM) and underinsured motorist (UIM) coverage are add-ons to your own auto insurance policy that step in when the at-fault driver either has no insurance or doesn’t have enough to cover your losses.

- Uninsured motorist (UM) coverage applies when the other driver has no insurance, or in hit-and-run situations where the at-fault driver can’t be identified.

- Underinsured motorist (UIM) coverage applies when the at-fault driver has insurance, but their policy limits aren’t enough to fully cover your damages.

Clear guide to California uninsured and underinsured motorist (UM/UIM) coverage

In California, insurers are required to offer UM/UIM coverage to every policyholder, but many people opt out to save a few dollars on their premium without realizing what they’re giving up.

In California, as many as 500,000 car accidents are reported per year, and the most recent data from the NHTSA (National Highway Traffic Safety Administration) states that a total of 40,901 people lost their lives in motor vehicle crashes in 2023.

Death is the worst possible outcome from a car accident, but not every family receives the same justice or compensation. Most California drivers are underinsured, with as many as 1 in 5 drivers having no insurance at all.

When pursuing compensation after a car accident, one of the most important, and overlooked factors in your payout is the at-fault driver’s policy limits. If the at-fault driver is uninsured, there may be nothing to recover at all, no matter how serious your injuries. That means you would have to pay for everything out of pocket alone.

Knowing your options before it happens can make all the difference.

California’s Insurance Requirements and the Gap They Leave

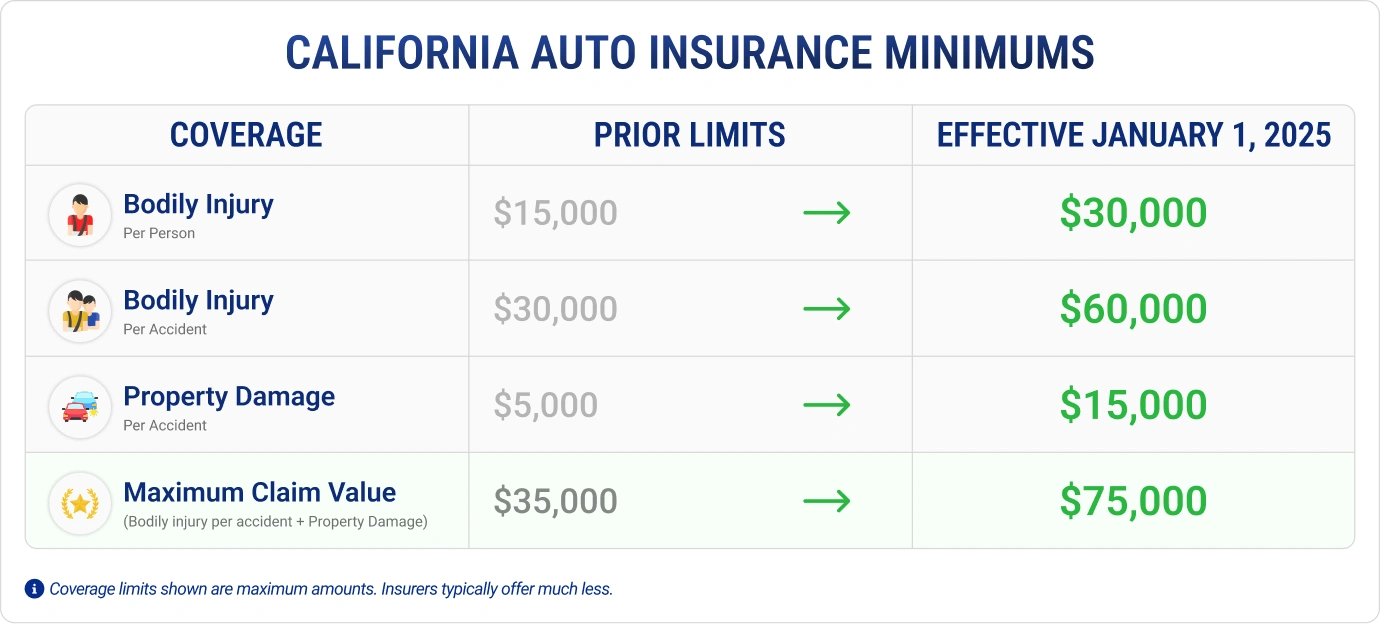

California law requires all drivers to carry minimum liability insurance. Previously, it was $15,000 for injury or death to one person, $30,000 per accident and $5,000 for property damage. Beginning in 2025, California’s minimum insurance limits for bodily injury and property damage were increased under SB 1107, the Protect California Drivers Act, with coverage amounts doubling to tripling from the prior minimum limits.

Here is an example scenario using California’s new 30/60/15 minimums, effective January 1, 2025. Keep in mind these figures represent the maximum potential payout. Insurers will typically offer far less, which is where legal representation becomes invaluable.

- Bodily injury per person: Each victim may claim up to $30,000; however, that amount is subject to a per-person limit within a shared policy pool. If there are three or more victims, the individual recovery for each claimant will likely be significantly less than the maximum amount.

- Bodily injury per accident: The $60,000 limit is the maximum available for all victims combined. Two victims may pursue $30,000 each. Three victims split it at roughly $20,000 each. Four victims at $15,000, and so on.

- Property damage: The $15,000 limit is separate from bodily injury but equally capped per accident, regardless of how many vehicles or properties are damaged.

Without UM/UIM coverage in California, an uninsured or underinsured at-fault driver may leave you with little to no compensation available for your injuries or damages. Even adding the minimum UM/UIM coverage to your policy can provide critical financial protection, making it one of the most important and affordable coverages you can carry.

These minimum policy limits are often far too low when considering how quickly medical expenses, lost income, missed work, and other accident-related hardships add up. As a result, many car accident victims are left in a difficult position: although the at-fault driver may be legally responsible for the damages, that legal responsibility does not guarantee meaningful financial recovery if the driver lacks sufficient coverage or assets.

You can sue an uninsured driver in civil court, and you may win, but collecting on a judgment against someone with no assets or income is often a dead end. This is where your own insurance policy becomes the most important tool you have.

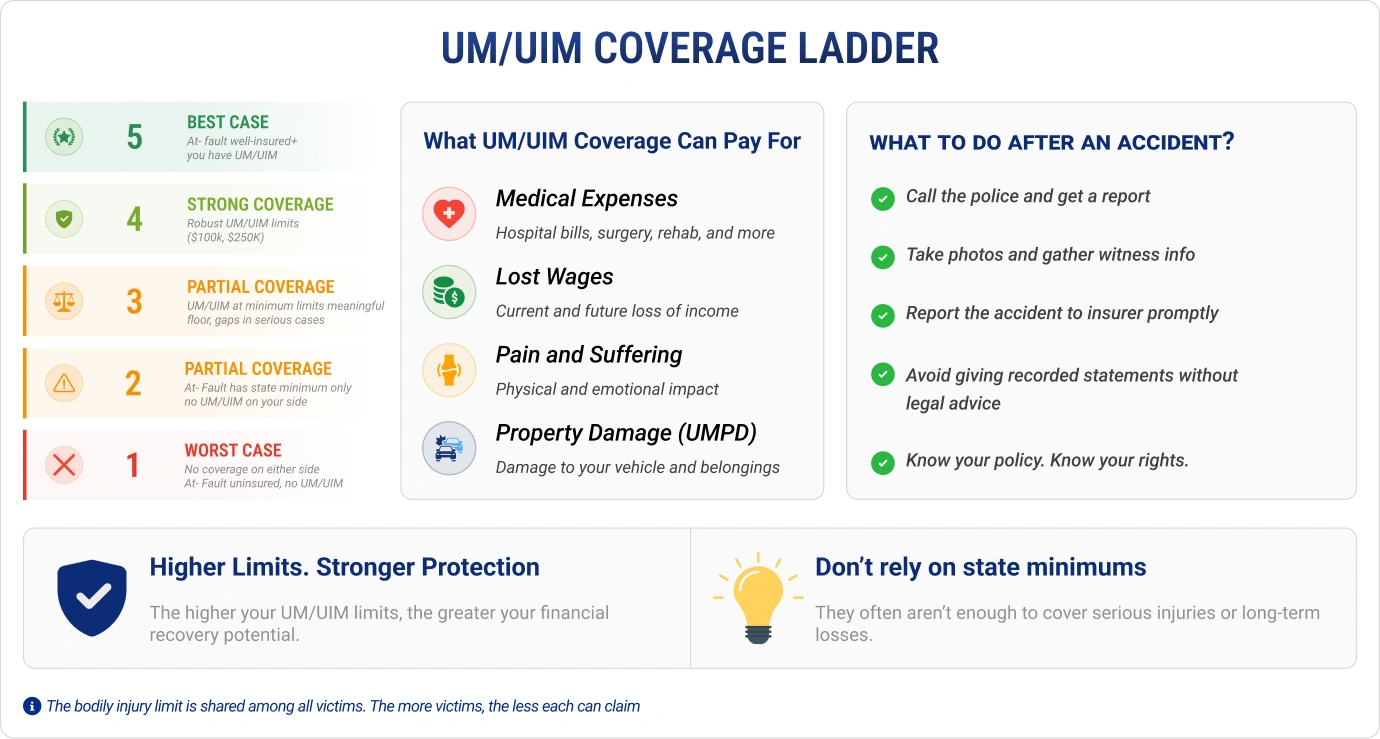

What UM/UIM Coverage Actually Pays For

UM/UIM coverage can compensate you for many of the same losses you’d pursue against an at-fault driver directly, including:

- Medical expenses (emergency care, hospitalization, surgery, rehabilitation)

- Lost wages and reduced earning capacity

- Pain and suffering

- Property damage (under uninsured motorist property damage, or UMPD, coverage)

It is important to understand that UM/UIM bodily injury coverage and Uninsured Motorist Property Damage (UMPD) are two separate coverages. UM/UIM helps cover injuries caused by an uninsured or underinsured driver, while UMPD helps cover damage to your vehicle or property caused by an uninsured driver. Having one does not automatically provide the other, so both coverages are needed to fully protect yourself in the event of an accident.

The coverage limits on your own policy determine the maximum amount available under your UM/UIM coverage. In California, prior to 2025, the minimum UM/UIM bodily injury limits were typically $15,000 per person and $30,000 per accident, meaning that was often the most an insured could recover through their own UM/UIM policy unless they carried higher limits.

For example, if a driver carries $500,000 in UM/UIM coverage, they may be able to pursue compensation up to those policy limits, depending on the facts of the claim and available offsets. This is also why large injury settlements and verdicts are often tied to higher insurance policy limits or substantial available assets.

Filing a UM/UIM Claim: What to Expect

Pursuing a UM/UIM claim means making a claim through your own insurance policy, but that does not necessarily make the process simple. Insurance companies, including your own carrier, still have a financial interest in limiting payouts. As part of the claim process, your insurer may request a recorded statement, challenge the extent of your injuries, dispute liability, or attempt to minimize the value of your claim.

A few things to keep in mind:

- Document everything at the scene. Get a police report, photograph the property damage, and collect witness information before leaving the scene.

- Report the accident to your insurer promptly. California policies typically have notification deadlines.

- Don’t give a recorded or written statement without legal advice. What you say early in the claims process can be used against you to reduce your settlement.

Why Legal Guidance Matters in Uninsured Driver Cases

UM/UIM claims are first-party claims, meaning you are pursuing benefits through your own insurance policy, but the process is often more adversarial than many people expect. Even though it is your own carrier, the insurer still has a financial interest in limiting payouts. During the claims process, they may request recorded statements, dispute liability, question the severity of your injuries, or attempt to reduce the value of your claim.

For that reason, having an experienced personal injury attorney can help you evaluate the full value of your claim, manage all communications with the insurance company, and push back when the insurer undervalues or delays resolution.

It is also important to be aware that while California generally provides a two-year statute of limitations for personal injury claims, UM/UIM claims can also be governed by policy-specific deadlines and contractual requirements that may be shorter. Understanding your coverage early can make a significant difference in protecting your rights.

Being hit by an uninsured or underinsured driver is stressful enough. Knowing how UM/UIM coverage works, and making sure you have adequate limits in place before an accident occurs, is one of the most practical ways California drivers can protect themselves on the road.